The third quarter of last year saw a slight uptick over Q2 in terms of new company incorporations, but it was still one of the slowest periods in the financial services industry’s recent history.

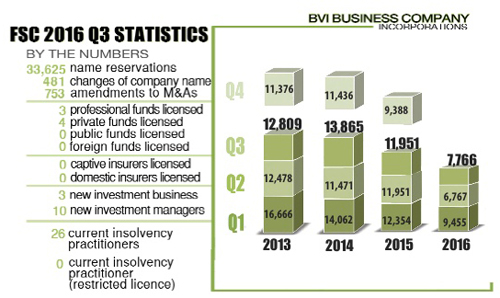

According to the most recent statistics from the Financial Services Commission, 7,766 new companies incorporated here in Q3 of last year. That makes the period the second worst quarter — second only to Q2 of the same year — for new company incorporations since at least 2003, when the FSC began issuing quarterly statistical bulletins.

According to the most recent statistics from the Financial Services Commission, 7,766 new companies incorporated here in Q3 of last year. That makes the period the second worst quarter — second only to Q2 of the same year — for new company incorporations since at least 2003, when the FSC began issuing quarterly statistical bulletins.

Moreover, last year is also on pace to be the slowest year for company incorporations since at least 2003, with just shy of 24,000 new incorporations through the first three-fourths of the year. By comparison, 21,111 new companies formed in Q4 of 2007 alone.

A silver lining in the latest quarter’s dismal numbers is that the total number of active companies in the Virgin Islands increased from 430,310 in Q2 to 447,503 in Q3. The number of active companies can increase despite a dearth of new incorporations because of previously inactive companies reactivating, according to industry professionals.

Gov’t revenue

Company incorporations are generally seen as a bellwether for the health of the territory’s financial sector, and they are the largest source of revenue for government.

During his budget address last week, Premier Dr. Orlando Smith said the slumping financial services industry led to a decrease in government revenue of about six percent through Q3 of last year. The industry typically contributes around $200 million to government coffers — roughly two thirds of total revenue.

Nevertheless, Dr. Smith said he is confident that the VI remains “an extremely attractive place to do business.”

“Whilst the number of new company incorporations has been impacted by factors such as bank de-risking, changes in global regulation and unprecedented levels of scrutiny and attention, we still proudly hold the position as one of the largest company incorporation jurisdictions in the world,” he said in a separate statement last Thursday, addressing the FSC stats.

Industry professionals largely seem to agree with Dr. Smith, but they continue to stress that the territory needs to act quickly on its plan to diversify the sector beyond company incorporation services.

“I think that we’ve been expecting a slowdown in incorporations for quite a few years now,” Kenneth Morgan, a longtime financial services professional and a current director of the fledgling Bank of Asia, told the Beacon on Tuesday. “The BVI is trying to reposition itself to maintain its incorporation levels while growing other services to ensure that current revenue and employment levels can continue.”

Harneys partner Jacqueline Daley-Aspinall spoke similarly, adding that the recent slump in company incorporations should serve as a “wake-up call” for the territory about the importance of diversifying its financial sector as soon as possible.

Contributing factors

Industry practitioners have cited the same reasons mentioned by the premier to explain the recent downturn in incorporation rates.

Last January, Vistra Managing Director Simon Filmer told a roomful of attendees at the BVI Business Outlook conference that many firms were hesitant to incorporate here because of regulatory uncertainty.

At the time, legislators were making changes to implement the global Common Reporting Standard, and they were also doing away with the longstanding “eligible introducer” regime, which allowed firms to keep company beneficial ownership information in other jurisdictions. Those changes have been implemented since then.

The territory’s image also took a beating last April when media outlets around the world started publishing stories on the Panama Papers, some 11.5 million documents leaked from the Panama-based trust firm Mossack Fonseca that allegedly suggested that VI-registered companies were used for money laundering and other illegal activity.

Some industry practitioners attributed the dismal Q2 numbers to the Panama Papers coverage, which began to appear two days after the quarter started.

“It’s hard to deny the timing connection between the decrease and the release of the stories,” Robert Briant, the managing partner of the VI branch of Conyers Dill & Pearman, said last October when the Q2 statistics where published.

‘De-risking’

The Panama Papers have also been blamed by some for international banks here ratcheting up their policies of “de-risking” — limiting their Caribbean operations or withdrawing from the region altogether over fears of “high risk” customers who might be engaging in money laundering and other criminal activity.

Indeed, documents obtained by the Beacon last July showed that at least 11 Panama-based trust firms were being denied banking services here, and the source who provided those documents painted the banks’ decision as a knee-jerk reaction to the Panama Papers.

“They’ve been told, ‘Listen, this has been a scandal. People are expecting some kind of a reaction from us. We need to see accounts closing,’” the source said at the time. “And they just decided to round up these accounts because they look like they’re connected to something that has been in the news recently.”

Financial Secretary Neil Smith agreed last October that the Panama Papers have impacted the ability of Panama-based firms to do business here.

“[The Panama Papers] has had a very visible impact on the bankability of Panamanian companies,” Mr. Smith said at the time. “It has affected our correspondent banking relationships. Whereas it was becoming problematic for over a year now, it was only after the Panama Papers that we’ve really felt the bite of that.”

‘New normal’

With industry practitioners such as Mr. Briant referring to the recent incorporation rates as a “new normal,” government has been exploring ways to diversify the financial sector beyond its typical company incorporation services.

Last September, BVI Finance announced that the Guernsey-based consulting firm Cutts-Watson Consulting Ltd. produced a report on the territory’s captive insurance sectors. Though officials declined to make the report public, BVI Finance said at the time that it lays out an implementation plan for attracting more business in the captive industry.

In November, the territory also saw the opening of the BVI International Arbitration Centre, which has been touted as a way to encourage more business here by offering a quick and efficient method to settle international commercial disputes.

At a press conference last month, Mr. Smith also said the VI is aiming to capitalise on new Organisation for Economic Cooperation and Development rules on “base erosion and profit shifting.” Those rules are aimed largely at ensuring that multinational corporations are taxed in the jurisdictions where they operate — meaning that the territory could benefit by having multinationals move staff here to justify having VI-registered companies.

However, Mr. Smith cautioned at the press conference that the VI needs to get its house in order if its wants to capitalise on BEPS. For example, he explained, it needs to undertake the usual gamut of initiatives officials often say are necessary to improve financial services, such as making it easier to get here, streamlining the work-permitting process, and improving physical infrastructure.

“In order to [capitalise on BEPS], we need to streamline the legislation and policies that exist in the BVI now to allow that to happen seamlessly,” he said at the time. “Because if things are simpler and quicker in another jurisdictions, then [companies] will go to that jurisdiction.”

{fcomment}